Blog

Identifying Solar Photovoltaic Tenders and Projects in Africa

by Alexandre Guillemot 5 min read

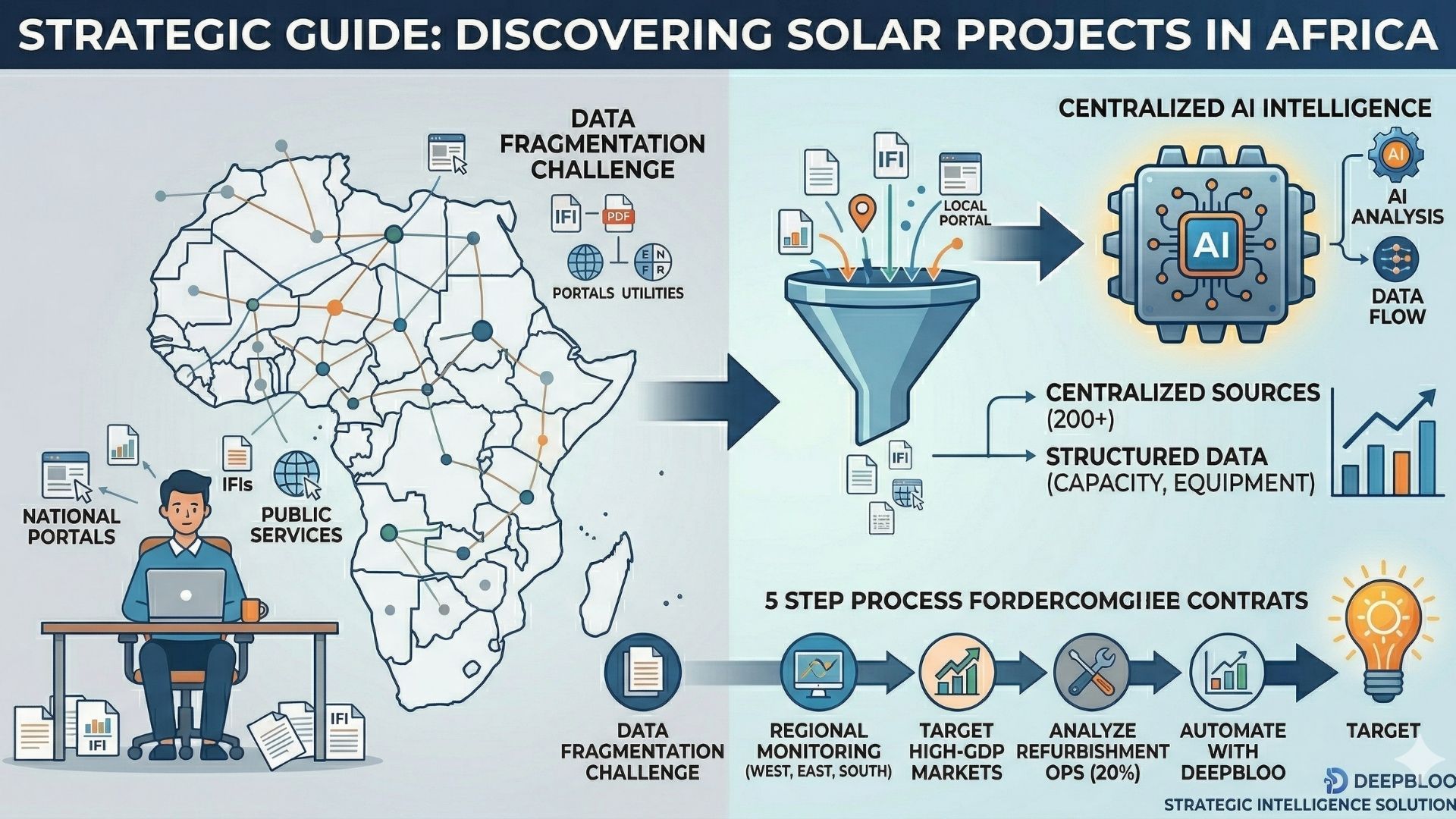

Identifying solar PV tenders in Africa requires a multi-layered monitoring strategy, as opportunities are fragmented across 200 different sources, ranging from International Financial Institutions (IFIs) like the World Bank to national utility portals and 54 distinct government procurement platforms. To understand the technology behind this massive data aggregation, you can explore how AI is revolutionizing tender monitoring in France and internationally.

The African solar market is entering its most transformative decade. While the potential for solar photovoltaic (PV) deployment is immense, the primary obstacle for developers, EPC contractors, and equipment suppliers remains the asymmetry of information. Unlike centralized markets, the African tender landscape is characterized by extreme decentralization, where a high-value project might only be published on a local ministry website or a specific donor portal.

1. Where to Find Solar Tenders in Africa: The Challenge of Fragmentation

Public procurement for solar energy in Africa is structurally decentralized, forcing companies to monitor three distinct “silos” of information to maintain an exhaustive pipeline. For those looking for a broader perspective beyond solar, we have developed a specific methodology on how to identify international tenders in the energy sector.

International Financial Institutions (IFIs) and Development Banks A significant portion of large-scale solar infrastructure is funded by the 35 major international organizations active on the continent. Key players include the World Bank, the African Development Bank (AfDB), and the French Development Agency (AFD). These organizations maintain their own procurement portals with specific compliance rules and publication schedules.

National Utilities and TSOs/DSOs National power utilities (e.g., ZESCO in Zambia, KPLC in Kenya, or ONE in Morocco) often launch tenders for grid-connected PV plants or network stabilization projects directly on their corporate websites. These technical tenders frequently bypass general government portals, making direct monitoring of utility sites essential.

National Procurement Portals Each of the 54 African nations has its own legal framework for public notices. Platforms such as Marchés Publics Morocco or Katika in Cameroon are vital sources, yet they often publish documents in non-searchable PDF formats or localized languages, creating a significant barrier for automated tracking.

2. 2025 Market Dynamics: Data-Driven Insights into African Solar Tenders

In 2025, an analysis of approximately 3,500 solar-related tenders published on the Deepbloo platform reveals a market driven by high-GDP nations and regional energy hubs. Navigating this complex landscape requires local expertise, which we detail in our post on how to identify international energy tenders in Africa: the complete guide.

The geographical distribution of these 3,500 tenders highlights the regions with the most active procurement cycles:

- West Africa: 1,092 tenders (The leading region for solar procurement)

- East Africa: 776 tenders

- Southern Africa: 757 tenders

- North Africa: 494 tenders

- Central Africa: 363 tenders

The highest volume of tender publications correlates directly with Africa’s largest economies, specifically South Africa, Kenya, and Nigeria, alongside emerging solar leaders like Tanzania, Ethiopia, Morocco, and Zambia. These countries leverage their higher GDP to de-risk investments and attract international funding for large-scale solar IPPs (Independent Power Producers).

Photovoltaic tenders in Africa - 2025

3. Scope of Work: Equipment, Installation, and Asset Life Extension

Solar tenders in Africa are no longer limited to new-build utility-scale plants; the market is diversifying into equipment supply, rural electrification, and the rehabilitation of existing assets. For technical firms, it is also crucial to know how to find engineering tenders in the African energy sector as it is for consulting companies to know how to find infrastructure and Renewable energy tenders in Africa

A breakdown of the 2025 tender data reveals the specific nature of the opportunities:

- Equipment Supply (50%): Half of all tenders focus on the procurement of hardware, including PV modules, inverters, and mounting structures, reflecting a massive push for localized assembly and distribution.

- Installation and EPC (30%): Nearly a third of the market involves full engineering, procurement, and construction services for new solar sites.

- Refurbishment and Maintenance (20%): A critical emerging segment involves the renovation, upkeep, or “refurbishment” of existing installations to ensure long-term grid stability and performance.

4. Deepbloo: Turning 200 Sources into a Single Solar Intelligence Feed

Deepbloo centralizes solar tender data from over 200 different sources across Africa, using AI to structure information from complex documents and provide a 360-degree view of the market. The manual tracking of 35 international donors and hundreds of local utility sites is a non-viable strategy for competitive firms. Deepbloo’s Semantic Engine scans technical annexes to identify “hidden” solar lots within broader rural electrification or urban infrastructure programs.

- Multilingual Support: Access tenders published in English, French, and Portuguese.

- Data Structuring: Extract power capacity (MW), surface area, and project status directly into Excel or your CRM.

- Early Detection: Identify “Weak Signals” from MRAE opinions or donor planning documents 12 months before the official tender.

5 Steps to Securing Solar Contracts in Africa

- Monitor the Big Three regions: Focus your commercial efforts on West, East, and Southern Africa, where 75% of the tender volume is concentrated.

- Target High-GDP Markets: Prioritize South Africa, Kenya, and Nigeria for consistent, high-value procurement cycles.

- Audit Refurbishment Opportunities: Don’t ignore the 20% of the market focused on maintenance and renovation, which often has lower competition than new-build EPC tenders.

- Track IFI Funding Pipelines: Follow the World Bank and AfDB project cycles to anticipate tenders during the “General Procurement Notice” (GPN) phase.

- Automate with Deepbloo: Eliminate manual searching and receive daily, qualified solar leads tailored to your technical capacity.

In Summary:

- Extreme Fragmentation: Solar tenders are scattered across 200+ sources; centralizing this data is the first step to competitiveness.

- Regional Leaders: West Africa and high-GDP nations like Kenya and South Africa dominate the 2025 landscape.

- Diverse Scope: Equipment supply represents 50% of the market, but refurbishment is a rapidly growing niche (20%).

- Data Integration: Use Deepbloo to transform administrative PDF noise into structured commercial signals.

Want to access the full database of 3,500 African solar tenders? Book a Deepbloo demo today.

Frequently asked questions

Which African region has the most solar tenders ?

In 2025, West Africa led with over 1,000 tenders, followed closely by East and Southern Africa.

Which donors finance the most solar projects ?

Approximately 35 IFIs are active, with the World Bank, AFD, and AfDB being the most frequent financiers.

What is the best way to track local tenders ?

Monitoring national utilities like ZESCO or KPLC and local platforms like Katika or Marchés Publics Morocco is essential for local market depth.

Can I find O&M (Operation & Maintenance) tenders ?

Yes, roughly 20% of current solar tenders in Africa focus on the refurbishment and maintenance of existing assets.